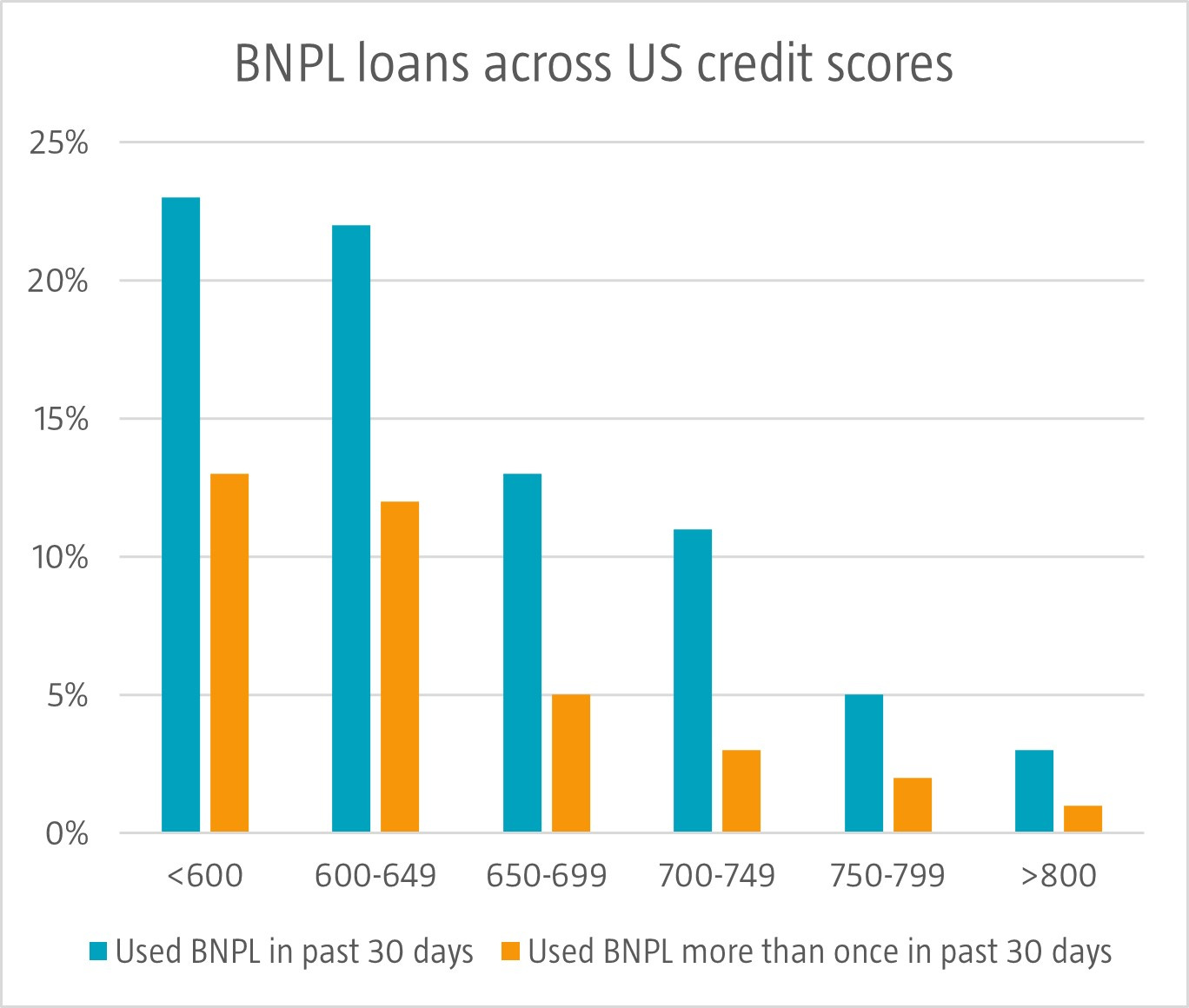

Using buy-now-pay-later (BNPL) services without impacting your credit score is no more for US consumers. FICO, the standard in US credit scoring used by 90% of top US lenders, now incorporates BNPL loan data. Although BNPL hasn’t been in the news as much as a few years ago, it’s a service that 15% of US Americans used last year according to US Federal Reserve data. Among all BNPL users, 24% paid late and this percentage is 40% among households earning less than USD 25,000. BNPL is more popular among consumers with lower credit scores. Data from the Boston Fed shows almost a quarter of those with a credit score below 650 used BNPL in the last month. Still, FICO and BNPL firm Affirm calculate that including BNPL data in FICO scores wouldn’t affect credit score much. The simulated inclusion of BNPL data into consumers’ credit scores had less than a 10-point impact for 85% of them.

Source: Federal Reserve Bank of Boston, 2024.